At the 2026 FIFA World Cup, 48 national teams will compete in the world’s largest soccer tournament. The U.S. will host 78 matches across 11 states, with an expected $11 billion in revenue and a record 6.5 million fans. FIFA has also approved an unprecedented $727 million distribution, including $655 million in prize money—a 50% increase over the 2022 World Cup—underscoring the significant tax stakes.

Hosting the World Cup raises a range of tax policy considerations— from balancing revenue collection and international competitiveness to administrative simplicity. At the same time, the tournament is expected to generate billions in economic activity as millions of visitors spend on hotels, restaurants, and transportation, producing tax revenue.

The tax treatment of this activity is shaped by federal tax law, state tax regimes, and bilateral tax treaties. The 2026 World Cup presents a multifaceted framework for taxation of global sporting events. Here are some of the issues shaping the tournament’s complex tax landscape.

Section 501(c)(3) tax exemption

While FIFA has been classified as a tax-exempt organization in the U.S since the 1994 World Cup, the organization has been unable to secure a similar exemption for its national teams until now. The Department of Treasury has reportedly made tax concessions, allowing national teams to apply for Internal Revenue Code (IRC) §501(c)(3) tax-exempt status. While not guaranteed, teams will be able to secure IRC §501(c)(3) status if they follow proper procedures. To be eligible, an organization must not benefit any individual private shareholders or take part in any political activity.

Nonresident individuals and tax treaty benefits

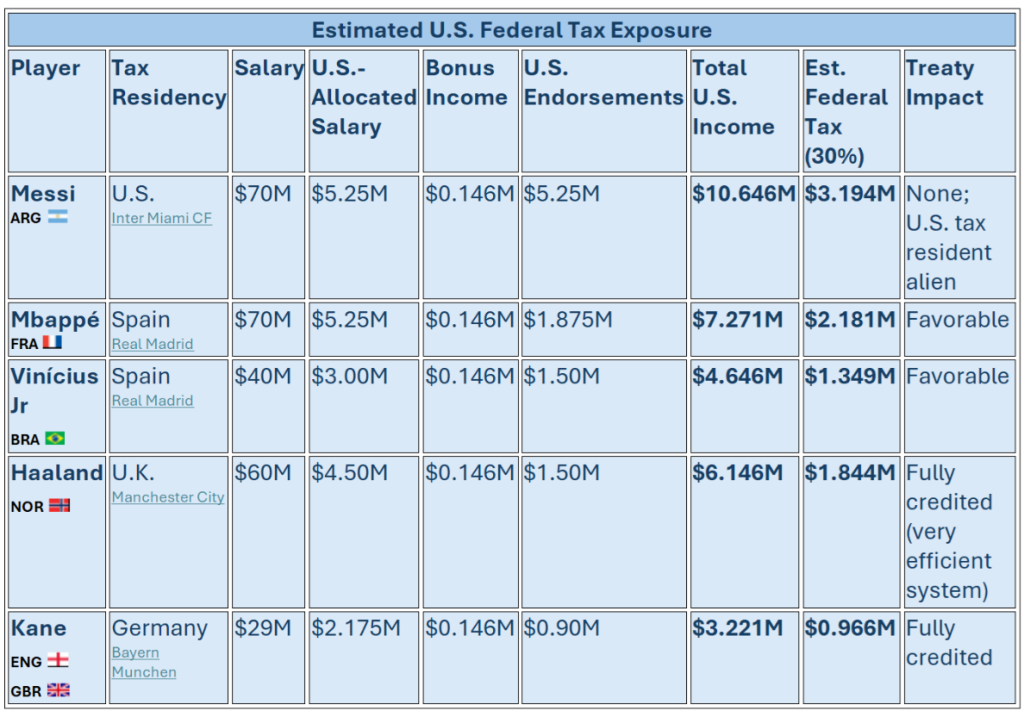

Athletes, coaches, and staff face both federal and state tax obligations on their income that is attributable to U.S. sources, unless exempt under a double tax treaty. For purposes of determining which double tax treaty applies, the country of tax residency is determinative. An Argentinian player that is a resident in Spain must rely on the U.S.-Spain treaty. Teams are required to withhold federal income taxes on U.S. source income paid to players and staff despite the federal exemption or a double tax treaty.

The U.S. has tax treaties with many countries that may reduce or eliminate U.S. tax or withholding, depending on the type of income and circumstances. Notably, tax treaties do not eliminate taxation; rather, they allocate taxing rights between countries to prevent the same income from being taxed twice. The most favorable treaties provide comprehensive double-tax relief through foreign tax credits or exemptions, reduce withholding tax rates on dividends, interest, and royalties, include clear residency tie-breaker rules to ensure predictable outcomes, broadly cover categories of income such as employment, business profits, and pensions, and provide efficient administrative procedures that enable taxpayers to claim treaty benefits with relative ease.

Additionally, all nonresident athletes are subject to a flat 30% federal tax rate, however treaties typically reduce or eliminate this tax on a reciprocal basis. Even if income is exempt from federal taxation through a double tax treaty, some states, such as New Jersey, do not recognize treaty exemptions for state income tax purposes.

U.S.-Canada prize money agreement

The Internal Revenue Service, Servicio de Administración Tributaria, and the Canada Revenue Agency have agreed to allocate FIFA prize money among the host jurisdictions based on the proportion of matches played in each country, thereby mitigating the risk of double taxation. Under the agreement, prize money is apportioned by multiplying earnings by the number of matches played in a jurisdiction and dividing that figure by the total number of matches played across the U.S., Canada, and Mexico.

The allocation methodology may also apply to payments by a national team to its athletes, independent contractors, and non-athlete employees, with the latter using a time-based allocation.

State and local income tax

The state and local tax liability of athletes and staff depends on the location of the team’s matches, the location of the team’s base camp, and tax treaties that are in place between the team’s nation and the U.S.

A so-called jock tax is imposed on athletes in states where they compete. For example, teams training in California face a jock tax at 13.3%. The number of “duty days” spent in California divided by the total number of “duty days” is multiplied by total annual income to calculate the portion of income subject to tax. Teams training in Florida or Texas are not subject to a state-level income tax or jock tax.

Enforcement challenges

Allowing participating national football associations to seek tax-exempt status under IRC § 501(c)(3) has raised concerns among host states regarding potential revenue losses. New Jersey tax officials, for example, have identified possible refund obligations for admissions, hotel occupancy, and sales taxes that might arise if exempt status is obtained. They also identified practical challenges in enforcing tax liabilities against foreign athletes and teams. With prize money being paid after participants have left the U.S., collecting tax can be difficult. New Jersey officials considered, but rejected as impractical, the use of jeopardy assessments to secure payment before prize money is distributed.

Biggest financial winner

FIFA is the economic “winner” of the 2026 World Cup, controlling the tournament’s most lucrative revenue streams—ticket sales and broadcasting rights. While the host cities bear much of the costs associated with event operations, FIFA has secured broad tax exemptions, allowing it to earn World Cup income free of taxation.

ABOUT THE AUTHORS:

Mina Capouet, JD, LLM, is a senior legal analyst at Wolters Kluwer Legal & Regulatory U.S. She specializes in compensation planning and employee benefits, with extensive experience analyzing and writing on the compliance and administration of qualified retirement plans, ERISA, group health, disability and welfare plans, and executive compensation. She also has expertise in state and local taxation, including individual income tax, sales and use tax, and credits and incentives. Mina earned a J.D. from Rutgers School of Law and an LL.M. in Taxation from Georgetown University Law Center and is admitted to practice law in New York and New Jersey.

Mavanee Anderson is a senior content management analyst at Wolters Kluwer Legal & Regulatory U.S. She specializes in estate taxation, U.S. bilateral tax treaties and international tax matters, providing legal analysis and editorial expertise on federal and cross-border tax issues. Prior to joining Wolters Kluwer, she held editorial roles at the American Payroll Association and Bloomberg BNA. She earned a J.D. from Vanderbilt University Law School, where she concentrated in international law.

Photo credit: FIFA/Instagram

Sign in to get access to this free resource, and all of our whitepapers and reports.

Download this content today!

Register Now Already registered? Click here to Log In

Tags: Canada, FIFA, fútbol, Mexico, soccer, sports, tax treaties, Taxes, united states, World Cup