The Public Company Accounting Oversight Board released a new publication on Thursday that highlights the results of conversations that board staff had with audit committee chairs of U.S. public companies and broker-dealers last year.

The audit committee chairs who were interviewed represent companies and broker-dealers whose audits are completed by PCAOB-registered accounting firms and reviewed by board inspectors.

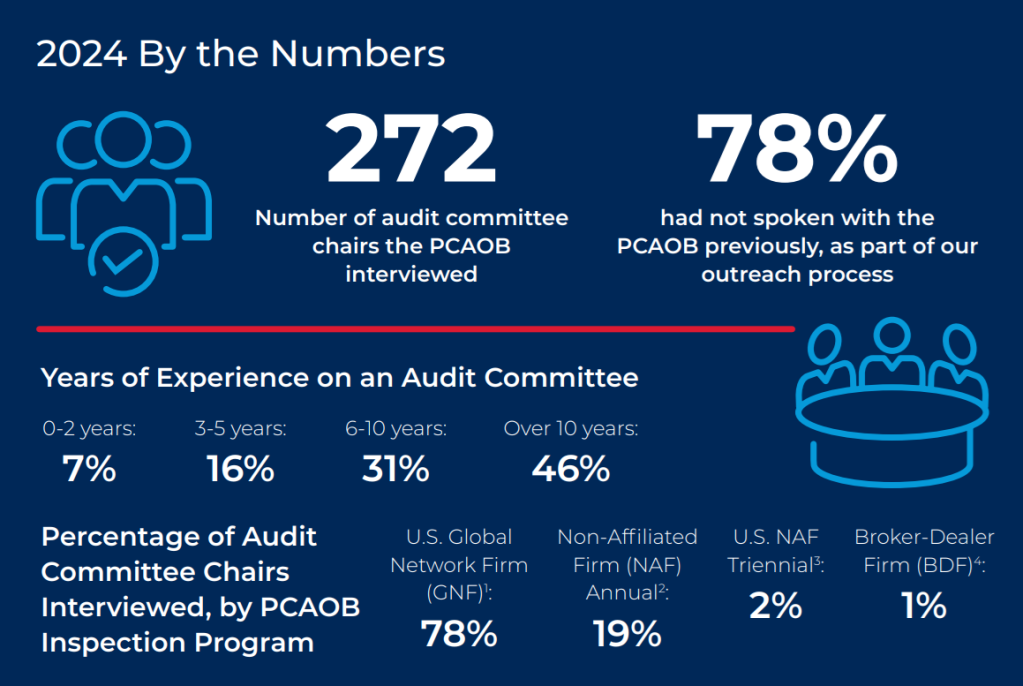

“Interacting with audit committee chairs provides critical viewpoints for PCAOB staff to consider in planning inspection activities,” the audit regulator said in a May 15 media release.

The publication, 2024 Conversations With Audit Committee Chairs, provides high-level observations and takeaways from the 272 interviews that staff conducted with audit committee chairs last year. Topics covered include—among others—factors affecting relationships with the audit firm, the economic environment affecting the audit, and the use of emerging technologies in the audit.

The publication also provides answers to questions that audit committee chairs regularly raise in their conversations with the PCAOB, such as:

- How are audits selected for review?

- What does an inspection entail?

- Does the PCAOB have educational training or events for audit committee members?

Key findings from the publication

Audit committee chairs described three factors they discuss with their audit firms that are vital to maintaining good working relationships with the firms. These factors included:

1. Communication: Most of the audit committee chairs interviewed identified transparent two-way communication as a key factor in ensuring the audit committee was well-informed of audit risks and areas of focus. The audit committee chairs interviewed noted that having an open dialogue, frequent meetings, easy channels of communication, or just being able to pick up the phone to call the audit partner were things that made communication between them and the auditor successful. In a few cases where the auditor was replaced, insufficient communication was identified as a key factor that led to the audit firm’s dismissal.

2. Coordination: Coordination between the auditor, management, and the audit committee was emphasized as vital for an efficient and effective audit.

3. Technical expertise: Another key element of interest was the level of technical expertise and experience of the audit team in the public company’s industry and the ability of the audit firm to retain personnel on the team with experience in the industry.

Most of the audit committee chairs interviewed said they review the PCAOB’s latest firm inspection report of their auditor and other information publicly available on the PCAOB website when determining whether to reappoint the auditor, the report states.

“Audit committee discussions with their auditors centered around key findings in the inspection reports and measures taken by the audit firms to address those findings,” the report says. “Certain audit committee chairs indicated that the inspection findings are typically summarized by the auditors for discussion with the audit committee. When the audit committee was considering changing audit firms, the audit committee chairs indicated that the findings in the reports were particularly important.”

In addition, approximately 63% of audit committees interviewed stated they had additional discussions, beyond the required communications, with their auditors related to the application to the audit and their financial statements of existing auditing or accounting standards.

The most frequently discussed topics included:

- Revenue recognition;

- Lease accounting;

- Current expected credit losses;

- Cybersecurity-required disclosures; and

- Securities and Exchange Commission’s climate-related disclosure requirements.

Audit committee chairs shared that critical audit matters were actively discussed during audit committee meetings. More than 60% of audit committee chairs interviewed indicated that CAMs inform stakeholders about topics that were a focus for the public company’s auditors, including the principal considerations that led the auditor to determine that the matter is a CAM and the procedures performed to audit the critical area.

“However, several audit committee chairs criticized the length of CAMs (wanting them to be briefer), the readability of CAMs, and ‘boilerplate language’ that was not specifically tailored to their public company,” the report says.

The report also notes that the expanded use of technology, including artificial intelligence, was a frequent point of discussion between audit committees and their auditors. Audit committee chairs said that while the use of technology has the potential to enhance the performance of audit procedures, it can’t replace the need for human oversight.

Sign in to get access to this free resource, and all of our whitepapers and reports.

Download this content today!

Register Now Already registered? Click here to Log In

Tags: Accounting, audit committees, Auditing, auditors, PCAOB