February 26, 2019

February 26, 2019

February 26, 2019

February 26, 2019

December 18, 2012

September 10, 2012

September 7, 2012

February 26, 2019

February 26, 2019

Red Wing Tax Forms is a standalone system for generating tax forms, and for filing taxes.

February 26, 2019

TaxCaddy is our next-generation 1040 productivity solution. TaxCaddy creates a tailored questionnaire and document request list to eliminate the cost and inefficiency of paper organizers. The questionnaire can be completed from any connected device. Documents like engagement letters and e-file authorizations can be e-signed. Your clients can use the TaxCaddy app for iPhone and Android...…

December 18, 2012

2013 Review of Tax Document Automation Systems

September 10, 2012

The IRS has announced emerging or significant areas that it will prioritize for the coming year. When it comes to compliance, the IRS has increasingly focused on small business underreporting, which is responsible for 84% of the $450 billion tax gap.

September 7, 2012

RedGear Technologies, known for its TaxWorks professional tax preparation suite, is now offering tools that tax firms can provide to their clients.

August 13, 2012

Beyond415 Added to Sage Accountants Network.

June 18, 2012

Even small businesses can benefit from sales tax automation, from the headaches of keeping up with constantly-changing rates, to the perils of audits and penalties.

November 16, 2011

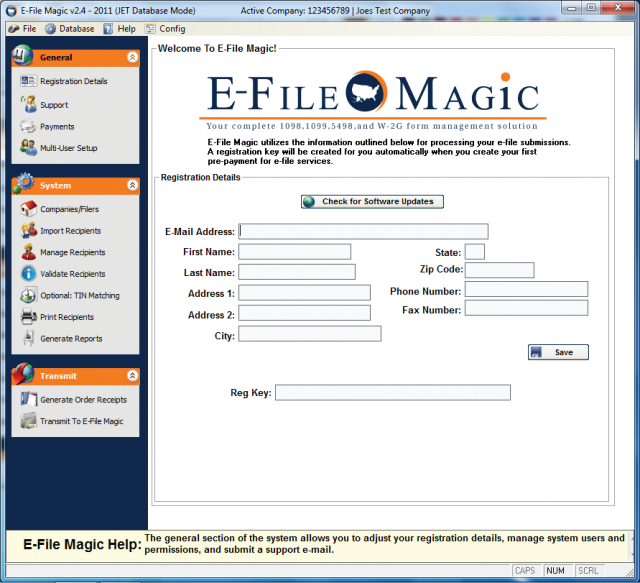

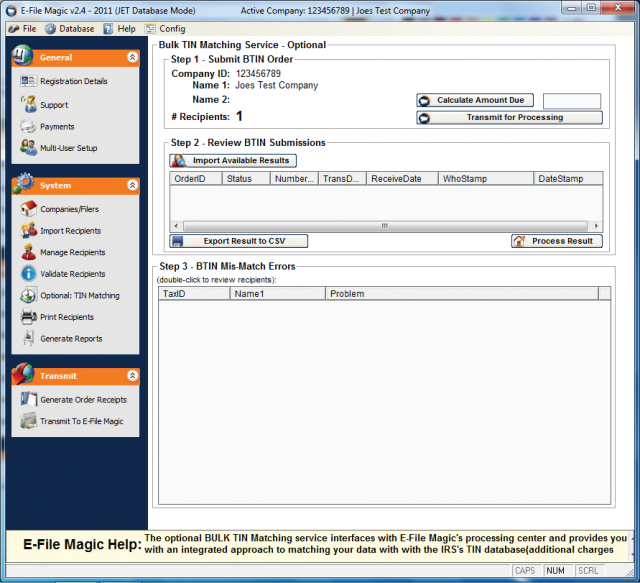

E-File Magic’s Bulk TIN Matching service provides you with an easy avenue to quickly submit your recipients/payees for TIN Matching with the IRS.

November 16, 2011

The E-File Magic 1099 from and e-File software you can print, mail, and e-file your 1099 Forms quickly and easily. You pay only for e-File Services(required), and optionally print and mail services. This makes your year end reporting requirements even simpler than ever. Just import or manually enter your data into our software program, validate,...…

November 16, 2011

Using the E-File Magic 5498SA software you can print, mail, and e-File your 5498SA forms with ease. Unlike our competitors we do not charge expensive licensing fees for our software. You pay only for e-File Services(required), and optionally print and mail services. This makes your year end reporting requirements even simpler than ever. Just import...…