April 14, 2016

CenterPoint Accounting Software

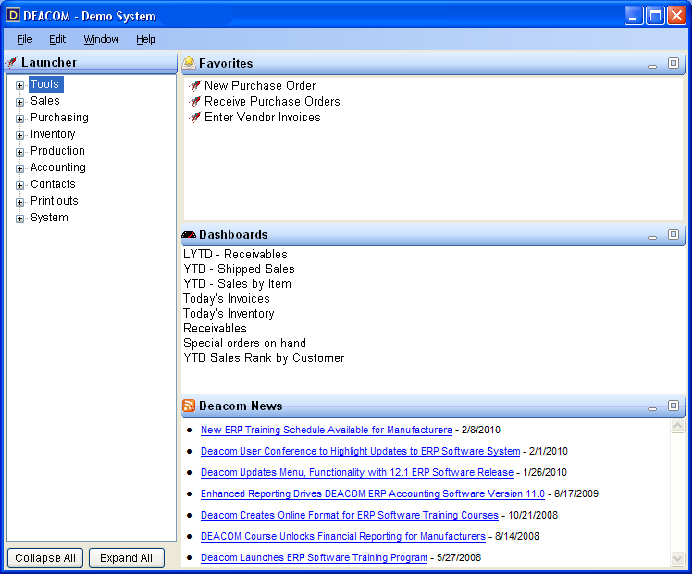

CenterPoint Accounting Software is solid financial accounting software with strong customization capabilities and reporting options. Better Data, Better Decisions. CenterPoint Accounting Software is a real-time accounting software application that allows businesses to track important information, so they can easily see which areas of the business are thriving, and which areas need improvement. CenterPoint Accounting...…