There’s so much nifty tax preparation software out there these days. Don’t you just love the software that allows us to import W-2 data, stock sales data, QuickBooks data, etc.? With all those tools, we barely even have to look at our clients’ documents. But we should!

TaxMama is a busybody. Otherwise known as a yenta. I always want to know everything about my clients’ lives – especially when it comes to their finances. Instead of looking at what my clients actually do, I look at what they don’t do.

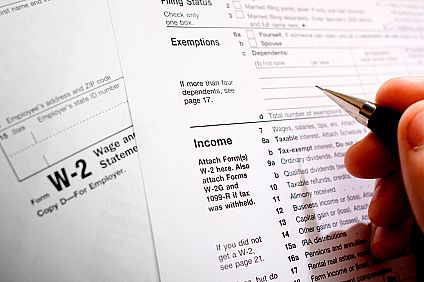

For instance, take a good look at the Form W-2. In fact, look at the instructions on pages 7 and 9 for boxes 10 and 12. It lists a variety of expenses that either reduced both taxable income and FICA/Medicare or just FICA/Medicare, among other things.

In box 10, I look for dependent care benefits. In box 12, I look for the following codes:

- D though H and S and Y – contributions to the employer’s retirement plan

- W – Health Savings Account contributions

In box 13, I look for the checkmark on Retirement Plan.

When those boxes are empty, I get excited. Why? I might have just hit the mother lode. Or…a small vein of gold.

The small vein? Ask your client if they don’t have retirement or cafeteria benefits simply because they choose not to participate. If that’s the case, become a hero and help your client understand the immediate value, the tax savings and the long-term benefits of these ‘tax loopholes.’ Yes, use that phrase. It makes them feel rich.

The mother lode? Aha! The employer doesn’t offer these benefits at all. Get your client to introduce you to the boss. Be prepared with a good, easy-to-understand visual presentation to show the boss just how much money the BOSS can save by offering these plans.

The cafeteria plan reduces wages – and all the related taxes on wages. The employer saves 7.65% on FICA/Medicare. They save money all other costs that are wage-based, like workers compensation insurance and other insurances. The employee saves their 7.65% of FICA/Medicare, as well as all federal and state taxes on their contributions.

The retirement plan contributions don’t cut anyone’s FICA/Medicare taxes. But they do cut the employer’s wage-based costs – WC, etc. And they cut the employee’s income taxes.

The administrative fees on these plans are generally lower than the tax savings.

Why a mother lode? Well, you become a hero to your clients, getting them tax breaks they didn’t have before. You show the employer how to save a ton of money – and give their employees an effective raise, without increasing their wages.

And you? You get a new client (the company), the boss, and even possibly other employees at the company. You can get a commission or consulting fee from the administrators of the plans. Or if you are in a position to sell and/or administer the plans yourself, you pick up all the extra fees from that, as well.

See – everyone wins because you looked past what was on the W-2 to what was missing.

———————————–

Eva Rosenberg, EA, is the publisher of TaxMama.com®, where your tax questions are answered. Eva is the author of several books and ebooks, including Small Business Taxes Made Easy. Eva teaches a tax pro course at IRSExams.com and tax courses to help you deal with tax debt http://www.cpelink.com/teamtaxmama.

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs

Tags: Income Taxes, IRS, Software, Taxes