Accounting

Internal Audit Functions Need Disrupting, Says PwC Study

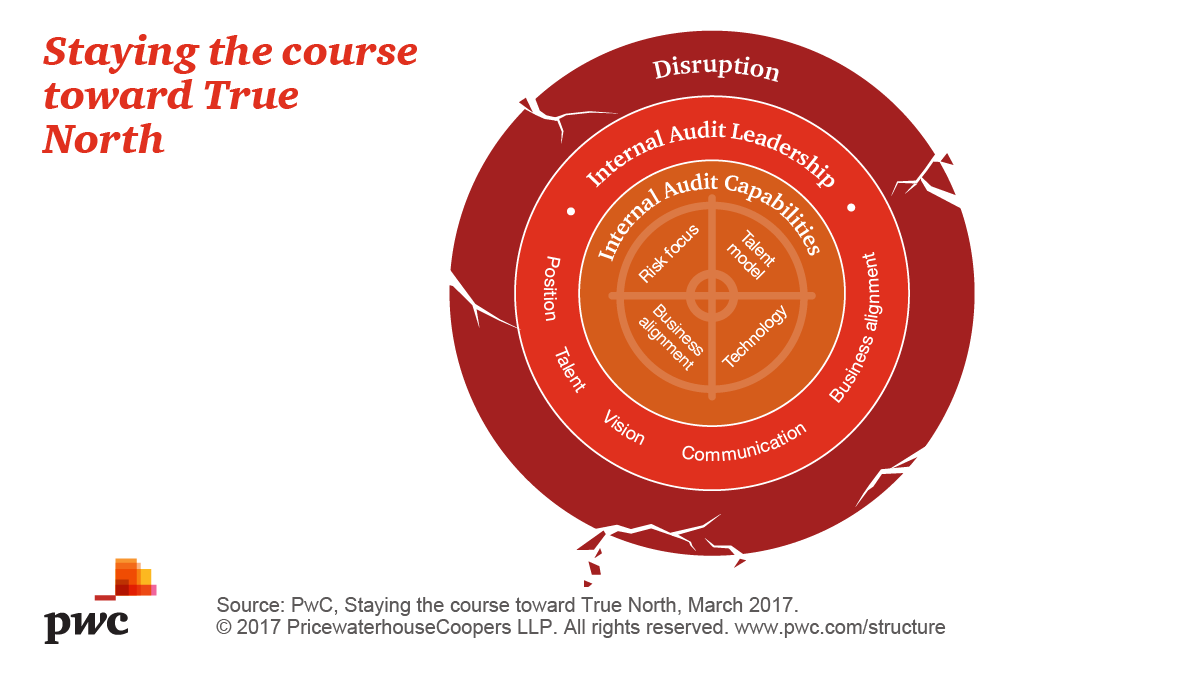

Internal audit functions are losing ground in trying to keep pace with stakeholder expectations, according to the 13th annual PwC State of the Internal Audit Profession study.

Mar. 29, 2017

Internal audit functions are losing ground in trying to keep pace with stakeholder expectations, according to the 13th annual PwC State of the Internal Audit Profession study.

This year’s study shows that the number of stakeholders that view internal audit as “contributing significant value” dropped from 54 percent in 2016 to only 44 percent in 2017, reaching its lowest level in five years. Despite this drop, the good news is that nearly half of all stakeholders want internal audit to take on a more integral role; this can be achieved through the function’s ability to help stakeholders better manage unplanned or unanticipated events, also known as market disruptions.

“Organizations are facing rising complexity of risks and new disruptive sources, impacting them at increasing speed. Stakeholders expect internal audit functions to help them navigate this changing landscape or face a shrinking perception of the value internal audit provides,” says Jason Pett, PwC’s US Internal Audit, Compliance & Risk Management Solutions Leader. “In a world of constant disruption, internal audit leaders need to think differently to accomplish more dramatic transformation and demonstrate their vitality. Particularly, they must be well-equipped to mitigate risk in several disruptive areas including regulatory changes, cybersecurity and changes to customer preferences — the disruptors most likely to impact businesses over the next three years.”

Based on nearly 1,900 respondents[1], 18 percent of them report that their internal audit functions play a valuable role in helping their companies anticipate and respond to business disruption – a subset of the pool which we’ve coined “Agile Internal Audit (IA) Functions.”[2] Nearly nine out of ten stakeholders with Agile IA Functions report that internal audit is adding significant value – that’s more than double the percentage of stakeholders with less agile internal audit functions.

The study uncovered two key traits that enable Agile IA Functions to lead in disruptive environments –preparedness and adaptiveness.

Preparedness

Agile IA Functions are forward-looking and able to identify emerging disruptions and associated business needs. They collaborate with other lines of defense in a unified and integrated manner and make decisions mutually supported by others in the organization. To boost preparedness, internal auditors should:

- Build the eventuality of disruption into planning and risk assessment: 84 percent of Agile IA Functions are mindful of disruption and include the possibility as part of the audit plan development, compared to 50 percent of less agile peers.

- Meaningfully collaborate with other lines of defense: 76 percent of Agile IA Functions cohesively work with other risk management and compliance functions to address disruption, compared to 40 percent of peers.

- Invest in and elevate business and technical IQ: 73 percent of Agile IA Functions provide Internal Audit with advanced technology and encourage the development of trending and analysis techniques, compared to 60 percent of peers.

Adaptiveness

Flexibility is key in Agile IA Functions—their processes must be transformative across audit plan development, audit planning, fieldwork and reporting. They should also use innovative talent models as needed and routinely reorganize or redirect resources according to disruption. To be adaptive, internal auditors should:

- Create more flexible processes and reporting mechanisms: 73 percent of Agile IA Functions change course and evaluate risk at the speed required by the business, compared to 37 percent of peers.

- Drive the use of data analytics and technology: 47 percent of Agile IA Functions have increased the use of data mining and data analytics for continuous auditing/monitoring of trends and potential impacts of disruption, compared to 35 percent of peers.

- Implement flexible talent models: 74 percent of Agile IA functions redirect/reorganize resources as needed to help the organization manage or respond to disruption, compared to 40 percent of peers.

“To become a leading internal audit function likely means changing what internal audit is doing and where it’s focusing, such as using more frequent proactive risk evaluations in advance of disruptions,” said Mark Kristall, Partner within PwC’s US Internal Audit, Compliance & Risk Management Solutions practice. “With an innovative vision of what internal audit can be, the function can deliver the greater value that stakeholders expect and need.”