Twenty-five top U.S. brokerage firms and insurance companies present their employees as trusted financial advisors putting client interests first even as their lobbyists argue in court that they are nothing more than commission-driven salespeople, according to a major new report from the Consumer Federation of America (CFA) and Americans for Financial Reform (AFR). The report also dissects how brokerage firms and insurance companies are systematically misleading unwary consumers.

Entitled “Financial Advisor or Investment Salesperson: Brokers and Insurers Want to Have It Both Ways,” (http://consumerfed.org/reports/financial-advisor-or-investment-salesperson-brokers-and-insurers-want-to-have-it-both-ways) the report written by Micah Hauptman and Barbara Roper, Consumer Federation of America, scrutinizes the websites for the brokerage firms and insurance companies and contrasts the practices they use to attract customers with those they use when resisting regulation as fiduciary advisers. It comes at a time when some in the brokerage and insurance industries are working feverishly, in court, on Capitol Hill and at Department of Labor (DOL) itself, to overturn a rule requiring financial professionals to act in the best interests of their clients.

Brokerage firms repeatedly, and in a variety of ways, characterize themselves as trusted advisors, while financial industry lobbyists argue in court that they are “merely selling a product.” The CFA/AFR review of prominent firms’ websites did not find on these firms’ websites any prominent reference that labeled their representatives and agents as salespeople. Instead, the firms have adopted titles for their financial professionals that identify those individuals as advisors:

* The title most commonly adopted by financial firms for their financial professionals appears to be “Financial Advisor.” Firms that use this title (or a variation of it) include: Janney Montgomery Scott, D.A. Davidson, Stifel, Wells Fargo Advisors, HDVest, Baird, Raymond James, Ameriprise, Edward Jones, BB&T Scott and Stringfellow, Chase, UBS, Morgan Stanley, SignatorOne (formerly John Hancock), Lincoln Financial, and VALIC.

* While “financial advisor” appears to be the title most commonly used by sales-based professionals, other firms have adopted variations that create a similar impression. For example, Schwab, Stephens, and Hilliard Lyons all use the title “Financial Consultant.” Hilliard Lyons also uses the title “Chartered Wealth Advisor.” Voya uses the title “Retirement Consultant,” USAA uses the title “Wealth Manager,” and Prudential uses the title “Retirement Counselor.”

Brokerage and insurance firms are so eager to attract clients and increase sales, they create the expectation that they are providing fiduciary investment advice rather than non-fiduciary investment sales. Here is how they do it:

* They routinely refer to their financial professionals not as sales representatives or agents but as “financial advisors” and indicate that they have a level of expertise that can and should be relied upon by their less sophisticated clients. In the in-depth review of company websites, researchers did not find one firm that referred to its financial professionals as salespeople.

* They typically describe their services as providing investment “advice” and retirement “planning,” not simply product sales. The CFA/AFR review of company websites did not identify any prominent description of their services as arm’s length investment sales recommendations.

* They market those services with messages whose clear intent is to convince retirement savers that they should trust that their advisor will be looking out for their best interests. In so doing, firms encourage reliance on their expertise and recommendations.

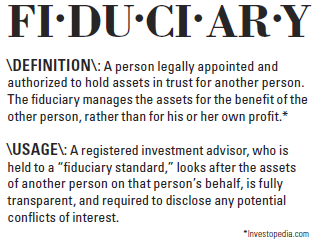

Barbara Roper, director of investor protection, Consumer Federation of America, said: “It comes down to this: are they financial advisors or are they just salespeople? Put another way, are they lying to the court, or are they lying to their customers? The answer to that question has multi-billion-dollar implications for millions of American workers and retirees who turn to financial professionals for help with their retirement investments. After all, people expect salespeople to look out for their own interests and maximize profits, but advisors are expected to meet a higher standard.”

Lisa Donner, executive director, Americans for Financial Reform: “Investors who unknowingly rely on biased salespeople as if they were trusted advisors can suffer real financial harm as a result. It is estimated, for example, that retirement savers lose $17 billion a year or more as the result of the excess costs associated just with conflicted retirement advice. The cost on an individual basis, in the form of lost retirement savings, can amount to tens or even hundreds of thousands of dollars over a lifetime of investing, money that retirees struggling to make ends meet can ill afford to do without.”

According to the new CFA/AFR report: “This (the positioning on industry websites of financial professionals) stands in sharp contrast to how financial trade associations have presented their business practices in legal filings challenging the DOL rule. In such filings, the U.S. Chamber of Commerce and several of its Texas affiliates, the Securities Industry and Financial Markets Association (SIFMA), the Financial Services Institute (FSI), the Financial Services Roundtable (FSR), the Insured Retirement Institute (IRI), the American Council of Life Insurers (ACLI), and the National Association of Insurance and Financial Advisors (NAIFA) have claimed, for example, that broker-dealer reps and insurance agents are not true advisors because they do not actually provide unbiased advice and are not engaged in relationships of trust and confidence with their clients. Instead, they claimed that broker-dealer reps are just ‘salespeople’ engaging in activity ‘whose essence is sales’ that is no

different from other commercial sales relationships in which ‘both parties understand that they are acting at arms’ length.’”

An earlier report from the Public Investors Arbitration Bar Association looked only at the advertising claims made by a smaller sample of brokerage firms and compared them to statements made by the financial companies in arbitration proceedings.

Micah Hauptman, financial services counsel, Consumer Federation of America, said: “Financial professionals who act like retirement investment advisers should be held to an advice-based standard, and that’s what the DOL rule does. Firms are sorely mistaken if they think they can continue the current charade in which they act like advisors to their customers while relying on their trade associations to argue the opposite in court in order to try to kill the DOL rule, they are sorely mistaken. People saving for retirement deserve to know where their advisor and the firm that their advisor works for stands on this issue.”

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs