Sales Tax

State Tax “Nexus” and Its Impact on Your Clients

All business owners want to operate a successful and growing business. Accomplishing this growth often requires entering new markets in different states. While these new states can offer exciting growth opportunities, they can also create various new ...

Apr. 06, 2015

All business owners want to operate a successful and growing business. Accomplishing this growth often requires entering new markets in different states. While these new states can offer exciting growth opportunities, they can also create various new tax obligations for the business. Determining whether these states have a legal right to tax your out-of-state business depends on whether your business has “nexus” with the state.

So, what exactly is Nexus?

For state tax purposes, the term “nexus” describes the amount and degree of business activity that must occur before a state can subject the company’s activities to income tax, and/or allow the state to require sales and use tax collection and remittance. The issue of nexus is complex because it involves the juxtaposition of constitutional law, federal and state judicial decisions, and state laws and regulations.

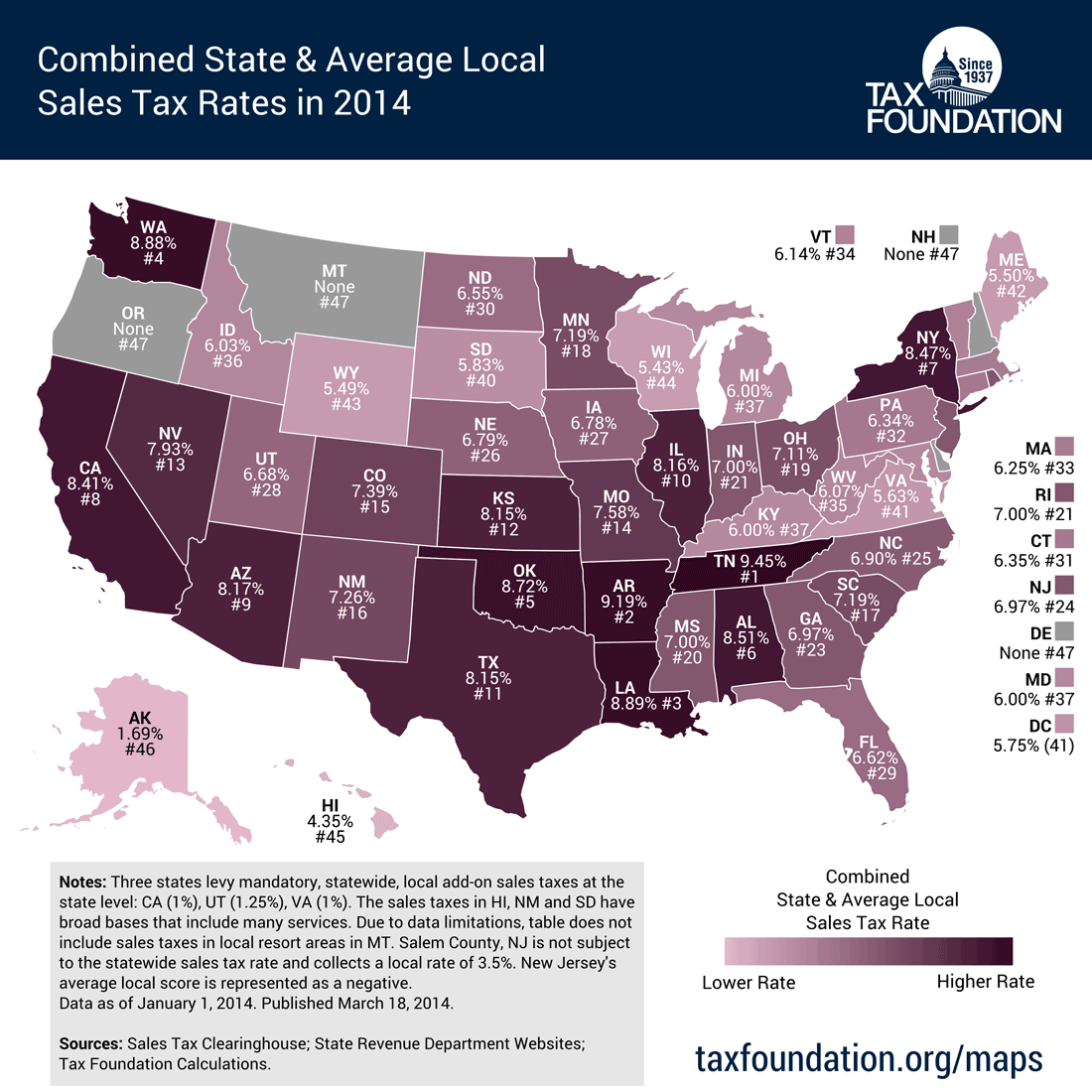

Sales Tax Nexus

In the landmark case Quill Corporation v. North Dakota, the US Supreme Court held that for purposes of sales and use tax, nexus means having “more than de minimis” physical presence in the state. Because the Quill Court did not define “more than de minimis,” most states have taken an aggressive viewpoint when interpreting the meaning. Not surprisingly, this has led to confusion and inconsistency among the states as to the amount and type of physical presence that gives rise to sales and use tax nexus. For example, some states will deem a company to have nexus if the only presence is an employee entering the state for a single day!

In general, the “more than a de minimis” physical presence standard can apply to either (or both) a company’s ownership of property (i.e., inventory) or personnel (i.e., employees and independent contractors) in a particular state. Most states do not provide any meaningful guidance as to the extent of the in-state physical presence required to create nexus. Absent a specific statutory rule, companies are left with interpreting a state’s administrative guidance and/or case law to make a nexus determination. Some states, however, have provided specific guidance depending on the type of property and/or activity conducted by the business in the given state. For example, certain states provide that employees attending in-state trade shows or conventions (without engaging in selling activity) less than a certain amount of days a year should not create nexus for the out-of-state business (assuming such business has no other contact with the state).

Income Tax Nexus

Since the Quill decision was specific to sales and use tax, there is a great deal of disagreement among the experts on whether the physical presence requirement applies to other state taxes, such as income tax. To no one’s surprise, most states say that the Quill decision is only applicable to sales and use taxes and, therefore, states may impose other tax types on businesses that don’t have physical presence in the state.

Benefits of a Nexus Study

Tax obligations vary from state to state, so understanding multi-state filing responsibilities is critical. States have gotten more aggressive with non-conforming companies, especially in today’s uncertain economic climate. Being fiscally motivated, the States are desperate to fill their coffers in order to pay for the services they provide. Also being politically motivated, they attempt to “export” the tax burden to out-of-state companies, who coincidentally, don’t get to vote in that state’s elections. Therefore, it is increasingly important for multi-state businesses to fully understand their state nexus “footprint.”

Nexus Studies analyze unique business practices while looking at how business is generated across the country. Depending on how a business is earning revenue, it might be subject to income, franchise, gross receipts, business activities taxes, and/or sales and use taxes (not to mention various registration responsibilities).

Watch a video on understanding sales tax nexus.

—————

Alexander Korzhen, JD, MBA, is State & Local Tax Manager at Eide Bailly LLP. The firm’s State & Local team provides Nexus Studies that help identify the various state tax filing and registration requirements. We work with our clients to identify how various tax standards apply to their unique business, advise them as they grow, and provide filing recommendations and strategies. Visit www.eidebailly.com to learn more.