By Wendy Walker.

In the last several years, the American workforce has seen a major shift in worker classifications. Sovos reported a 33% increase in 1099-K forms filed from the tax year 2020 to 2021, and a 17% increase in 1099-NEC tax forms, both signaling a significant increase in gig and contract work. With new tax reporting requirements taking effect in 2023, it is imperative that SMB owners understand the tax implications of those recent workforce changes, as well as the practices for managing any new tax obligations.

Below are six tips to help SMB owners tackle the latest updates in tax reporting and filing thresholds:

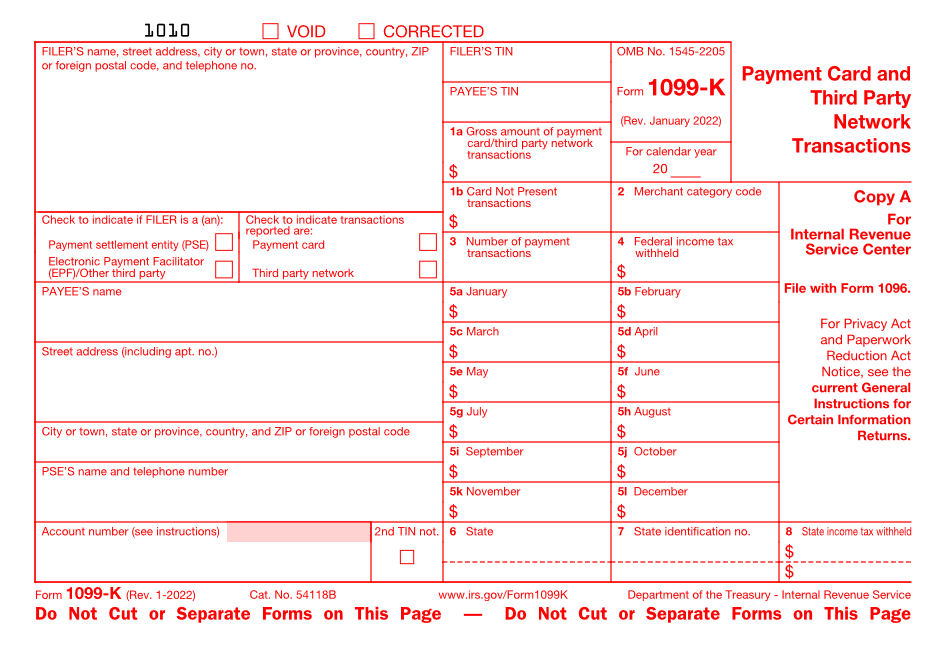

- Be prepared to receive a 1099-K – maybe for the first time. The IRS reporting threshold has dropped for Forms 1099-K, which means online platforms will be issuing forms for anyone with transactions totaling more than $600. Closing the tax gap is a high priority, as evidenced by the $80 billion the IRS received in the Inflation Reduction Act this year, more than half of which is earmarked for enforcement. Small business owners will need to be vigilant about compliance.

- Be mindful of gross amounts reported on 1099 forms. If a small business is using online platforms to source work, they’ll need to be mindful of the discrepancy in the gross amounts reported on Forms 1099-K vs what they actually received from the platform company. The amount reflected on their 1099-K likely includes business-related expenses including fees and credits. Small businesses should get a copy of all the transaction details that make up the amounts reported on the 1099 so that they can properly identify and account for deductible business expenses.

- Don’t use business accounts for personal transactions. Online platform systems cannot distinguish between personal and business transactions – which means the 1099-K they report could include amounts that aren’t even business related. And, when amounts reported by third parties on 1099s don’t match amounts reported by the small business on their income tax return, it can cause a red flag with the IRS (and states) and even lead to unnecessary penalty notices. While taxes aren’t due on those personal transactions, the headache of proving that out isn’t worth the risk.

- Remember the Increased volume of tax reporting forms: With the IRS lowering the threshold to report earnings and payment transactions for gig workers, freelancers and contractors, businesses must now complete hundreds of thousands more tax forms by January 31, 2023. Be prepared for the delays this is likely to cause and don’t expect anything to happen quickly.

- Missing or incorrect information can be very expensive: Improper tax documentation collection and validation processes often lead to incorrect information being reported on tax forms, which can lead to incorrect filing penalties and trigger withholding obligations for organizations, amounting to $280 per form, with a cap of about $3.4 million.

- Zelle is not the same as Venmo. Zelle is an ACH payment network. Banks partner with Zelle to participate in the network and if your bank participates, you can use it to transfer funds via ACH to participating bank accounts. ACH networks are not subject to 1099-K reporting. Venmo is a digital wallet like PayPal- you can store money in your account, and you can reload the Venmo account with funds from various sources like credit cards, and you can transfer money out of your Venmo account to other digital wallets. Venmo is considered a third-party payment network for 1099-K reporting purposes.

======

As a solution principal for Sovos, Wendy Walker uses her market expertise to create and implement product and solution strategies that help customers meet the demands of a constantly changing regulatory environment. Since joining Sovos, Wendy has helped lead the go-to-market strategy focused on growing the Tax & Regulatory Reporting line of business.

Sign in to get access to this free resource, and all of our whitepapers and reports.

Download this content today!

Register Now Already registered? Click here to Log In

Tags: Payroll, Payroll Taxes