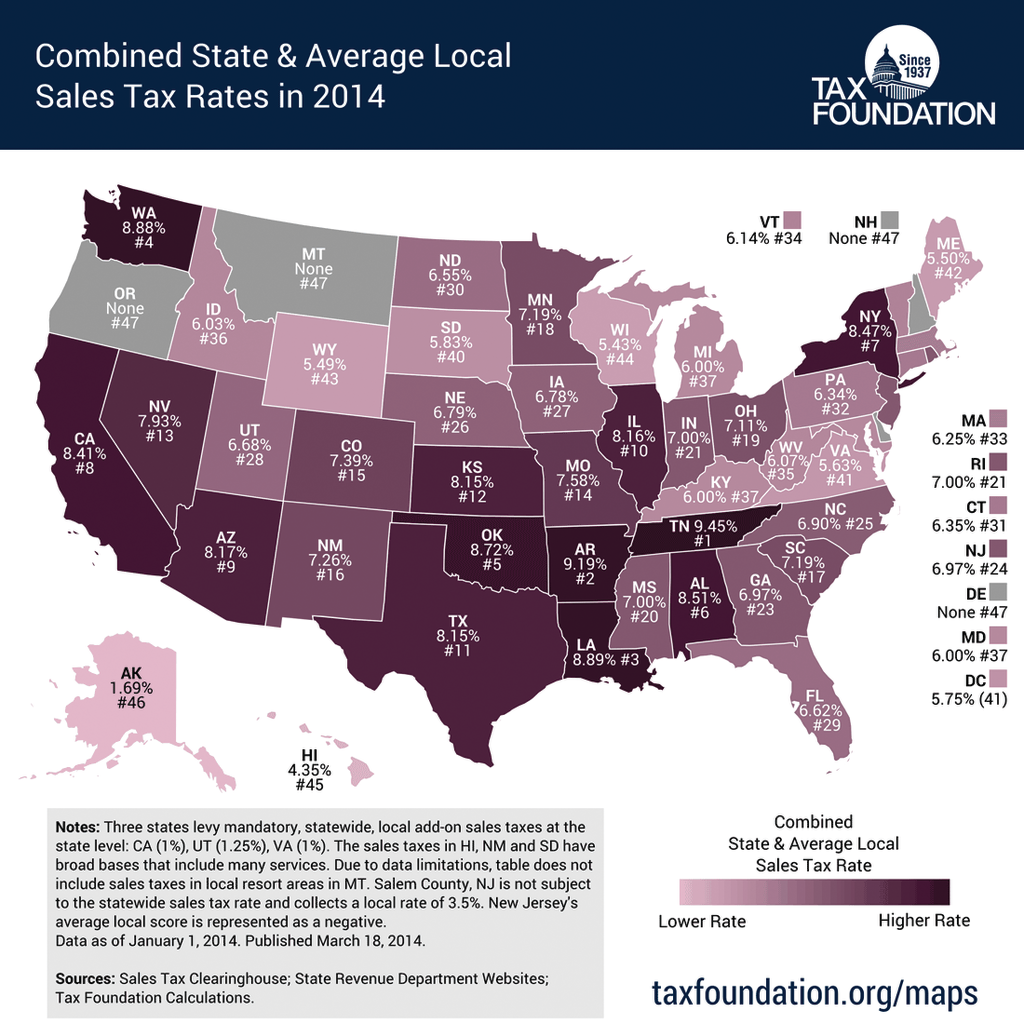

Sales Tax

Talking to Your Clients About SALT

The Year in the Life of a State and Local Tax (SALT) Accountant series is being created with the practitioner in mind. In cooperation with Avalara, each month we'll provide you with the latest news relating to state and local tax issues, updates on federal legislation, checklists and tips for building and improving your SALT practice, talking points and guidance for answering the questions posed by your clients, and more.

Jun. 06, 2014

Introduction to SALT Series:

The Year in the Life of a State and Local Tax (SALT) Accountant series is being created with the practitioner in mind. In cooperation with Avalara, each month we'll provide you with the latest news relating to state and local tax issues, updates on federal legislation, checklists and tips for building and improving your SALT practice, talking points and guidance for answering the questions posed by your clients, and more.

We'll work with both seasoned SALT accountants and those who are new to this area of practice so you can learn what others in the field are doing. We welcome your comments, questions, suggestions, concerns, case studies, guest articles – please participate with us as we enter and share with you the lives of state and local tax accountants.

— Gail Perry, CPA, Editor-in-Chief, and former SALT accountant

Even those accountants who don't specialize in sales and local taxes or are without a SALT (State and Local Tax) practice, can guide clients on the current environment around sales tax compliance. The combined effect of growing untapped online-sales-related tax, and persistent state budget shortfalls has sparked legislative initiatives at both the state and federal levels.

Here are some basic questions accountants can ask clients and some suggested guidance you can provide on these important compliance issues.

Background:

Since the early 1990s, states have primarily relied on definitions of nexus the relationship between an entity and a taxing jurisdiction that triggers a tax obligation. Nexus has usually been defined as “significant physical presence” in a taxing jurisdiction. Under this definition, employees, warehouses, and headquarters constitute “significant physical presence.” Besides that tangible physical presence, depending on the rules of the individual state, other activities and connections a vendor has within a state including attending trade shows or conferences, or utilizing remote employees in the state may trigger nexus.

These activities and connections lie at the heart of the current debate. Today, a seller whose activities and connections within a state do not establish nexus is not obligated to collect and remit sales tax in that state. Online retailers like Amazon, Overstock, eBay, etc. that aren't required to charge customers sales tax have caught the attention of states seeking revenue to fill budget shortfalls. Over the past several years, members of Congress and state legislators have grappled with whether to require Internet retailers without physical presence in a taxing jurisdiction to collect sales tax. Last year the Senate passed the Marketplace Fairness Act, (69 to 27); a bill that, if passed by the House, would grant states the authority to tax remote sales. This legislation will apply to all types of remote sellers,including Internet retailers, catalog companies, and similar vendors.Consequently states would then have the authority to tax many remote sellers who have escaped the obligation to collect sales taxes in the past.

Questions your clients may ask about the Marketplace Fairness Act:

- I sell over the Internet today. Will I be affected if this legislation passes?

- Does it make a difference what I'm selling over the Internet?

- What if my remote sales are less than $1 million annually?

- Does this bill still apply to me?

Will all remote sellers be affected?

As passed by the Senate, companies with total remote sales over $1 million (including exempt sales) could be required to collect sales tax. Typical to the legislative process, this threshold is a moving target and may change before the bill passes the House. With this in mind, companies should proceed with normal planning for sales tax compliance.

If passed, states must adopt revisions before they can enforce sales tax changes.

While some clients might panic and think that passage of legislation will trigger immediate changes to their sales tax collection responsibility, implementation will vary widely by state, depending on each state's legislative process and ability to comply with minimum simplification requirements.

The Senate version allows the 23 states that are full members of the Streamlined Sales Tax an easier path to implementation, although still requires the 90-day waiting period. For the other 22 states and the District of Columbia, implementation of this law will take longer – at minimum 6 months.

Currently, national legislation is only one part of the sales tax compliance puzzle. Affiliate Nexus?

Regardless of what happens at the federal level, and perhaps nothing has happened at the Federal level yet, states are making their own legislative changes that are in some cases more aggressive than those proposed in MFA. States are setting up nexus rules around affiliate nexus or so-called “Amazon Laws.” These are enough to keep compliance experts busy for years.

Affiliate nexus laws come in two forms:

- In-state websites: In this version, an in-state company or organization (entity) places on its website a link to an out-of-state retailer and the out-of-state retailer agrees to pay a commission to the in-state entity anytime someone clicks on that link and buys something from the out-of-state retailer. The states claim that the in-state entity is the agent of the out-of-state retailer and therefore constitutes a sales tax collection responsibility.

- In-state warehouses: With these, the state law says that an in-state warehouse that is part of a consolidated group of companies (states use the IRS definition) with the out-of-state retailer creates physical presence for the out-of-state retailer. Under this concept the states pierce the corporate veil and ignore that the two companies are separately incorporated.

Some call these “Amazon laws” because many who support them are trying to attack the way Amazon conducts business, even though there are plenty of other companies that operate this way.

In the past three years, many states have adopted Amazon Laws – state laws that require Amazon and other out-of-state sellers to collect sales tax for the first time.